Income-Splitting for Private Companies

The Government of Canada has proposed technical rule changes that will reduce the tax benefits of income-splitting using private corporations, effective January 1, 2018.

Background

Opportunity: Canada’s tax system is designed based on the principle of integration, wherein income earned by a corporation and distributed to shareholders via dividends should be subject to the same tax as if it was earned directly by an individual via a salary. In other words, there should be no tax consequence to incline people to operate with a corporation over without one, or to pay dividends or salary over the other. Although a positive theory, differences in the top personal and corporate rates make perfect integration complex and hard to achieve.

Motivation: Income-splitting is motivated by Canada’s graduated personal tax rates (i.e. the more you earn, the higher your rate) vs. lower corporate rates. A family’s overall tax can be reduced by using a corporation to defer tax and shift income from a higher-income family member to a lower-income one. One common method is to issue shares of the corporation to family members, then pay dividends out to all shareholders. Adult children attending school often pay zero tax on those dividends due to their low tax bracket and other special tax credits they receive.

Why the Change?

Historically, the government has allowed income-splitting via dividends as a perk for small businesses, and even created other provisions that treat the family as one economic unit. For example, a higher-income spouse can contribute to a Registered Retirement Savings Plan on behalf of a lower-earning one and the Goods and Services Tax Credit is calculated using family income. If the family was the basic tax-paying unit, there would be no point to enacting rules against income-splitting. However, the current Liberal government, elected in 2015 largely with the support of younger voters who are less wealthy and less likely to own businesses, favours the view of an individual-based tax system rather than family-based. This government has also argued that over time, many high-income earners took advantage of the system and incorporated just to avoid paying their fair share. The new legislation is aimed in fairness to maintain a neutral tax system between employees and the self-employed who use corporations.

Proposed Legislation

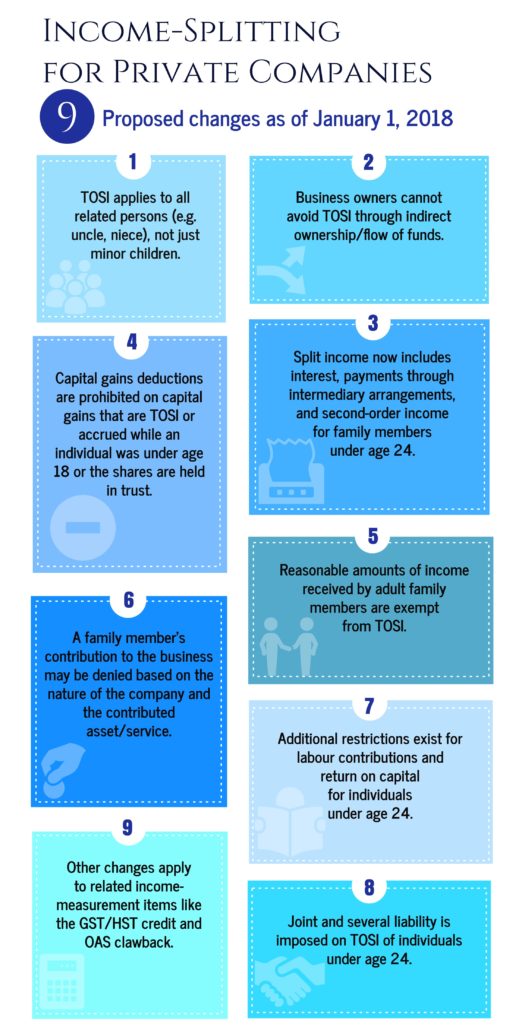

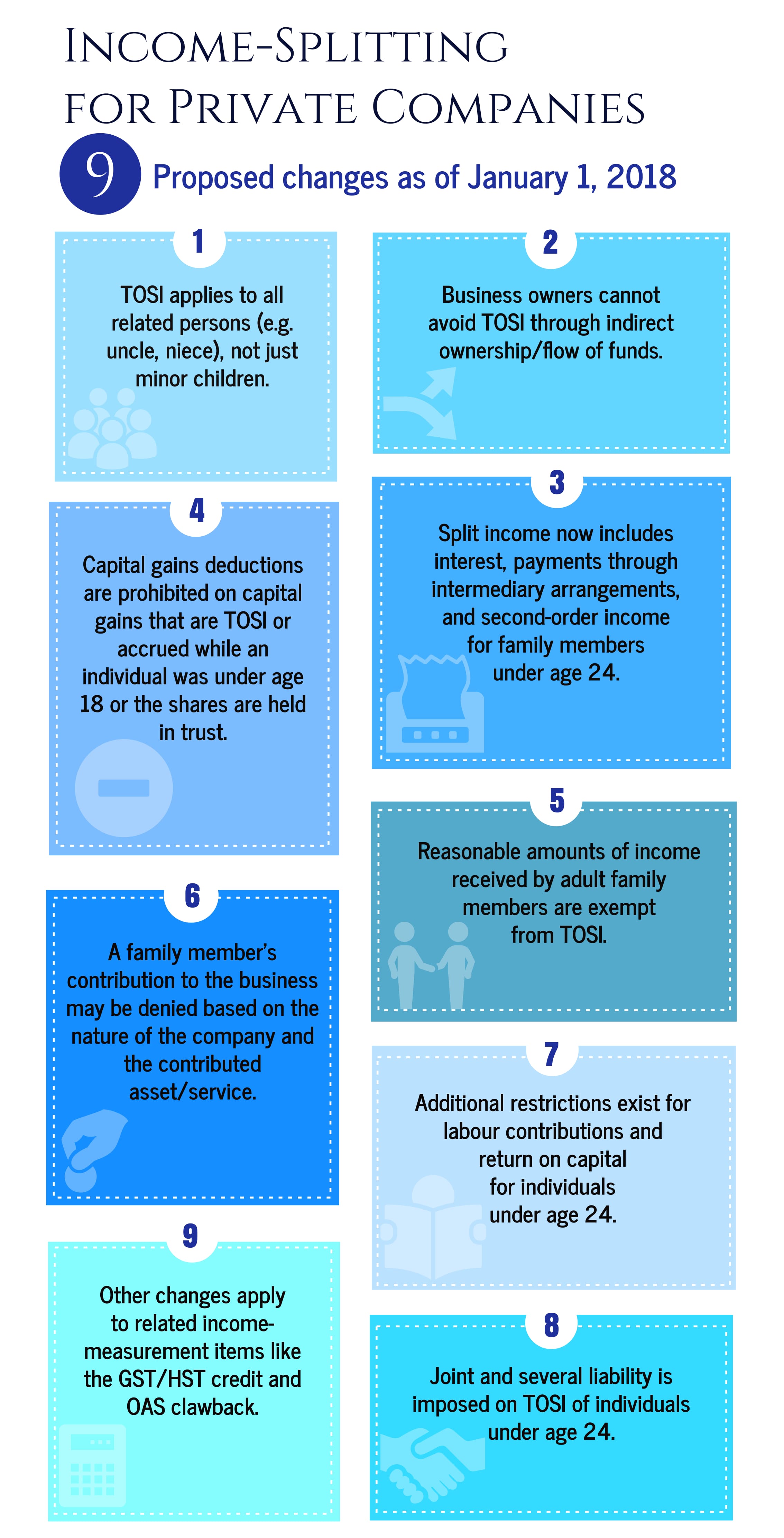

The current law subjects children under the age of 18 to tax on split income (“TOSI”) at the highest marginal tax rate. Split income is defined as almost any type of income received from non-publicly traded entities other than salary or business income. The proposed revisions include the following:

- Application of TOSI not just to minor children, but to anyone related to the income-generator (e.g. uncle, niece, etc.) and who receives income derived from his/her business, partnership, trust, etc.

- Expanded definition of who is the income-generator to make it more difficult to avoid this status through indirect ownership or an indirect flow of funds.

- Broader definition of split income to include interest and payments made through intermediary arrangements as well as second-order income for family members under age 24 (i.e. subsequent income earned on original income that was caught under the split income rules).

- Prohibition of capital gains deductions with respect to capital gains that are TOSI or accrued while an individual was under age 18 or the shares are held in a trust.

- Exemption from TOSI of reasonable amounts of income received by adult family members (e.g. if his/her labour contribution is worth $50,000 and he/she receives a $60,000 salary, TOSI only applies to the excess $10,000).

- Denial of family members’ contribution (and thus the right to receive income) if the business’ principal purpose is to derive income from property or the contributed asset was financial assistance like guaranteeing a debt.

- Additional restrictions on the labour contribution and return on capital for individuals under age 24.

- Joint and several liability (i.e. full responsibility) of the income-generator for TOSI of individuals under 24.

- Changes to related income-measurement items (e.g. GST/HST credit, Old Age Security clawback, etc.).

The proposed law is still under discussion and it’s likely that more revisions are coming! Attached is a Guide on Income-Splitting for Private Companies. Contact us today to find out what you can expect and how to prepare your company and family for what’s ahead.