Taxation of Insurance for Corporations

Taxation of Insurance for Corporations

If you’re incorporated, you might be wondering what the implications are of paying insurance premiums and collecting benefit proceeds through your corporation. Or perhaps you are considering offering employee benefits like life, disability, and extended health and dental insurance coverage as a way of attracting and retaining quality personnel. As accountants, we’re starting to see the same question come up time and time again:

“How is insurance treated for tax purposes in corporations?”

We always recommend seeking personal tax advice for your specific situation. But if you’re looking for some general guidance, here’s what you need to know…

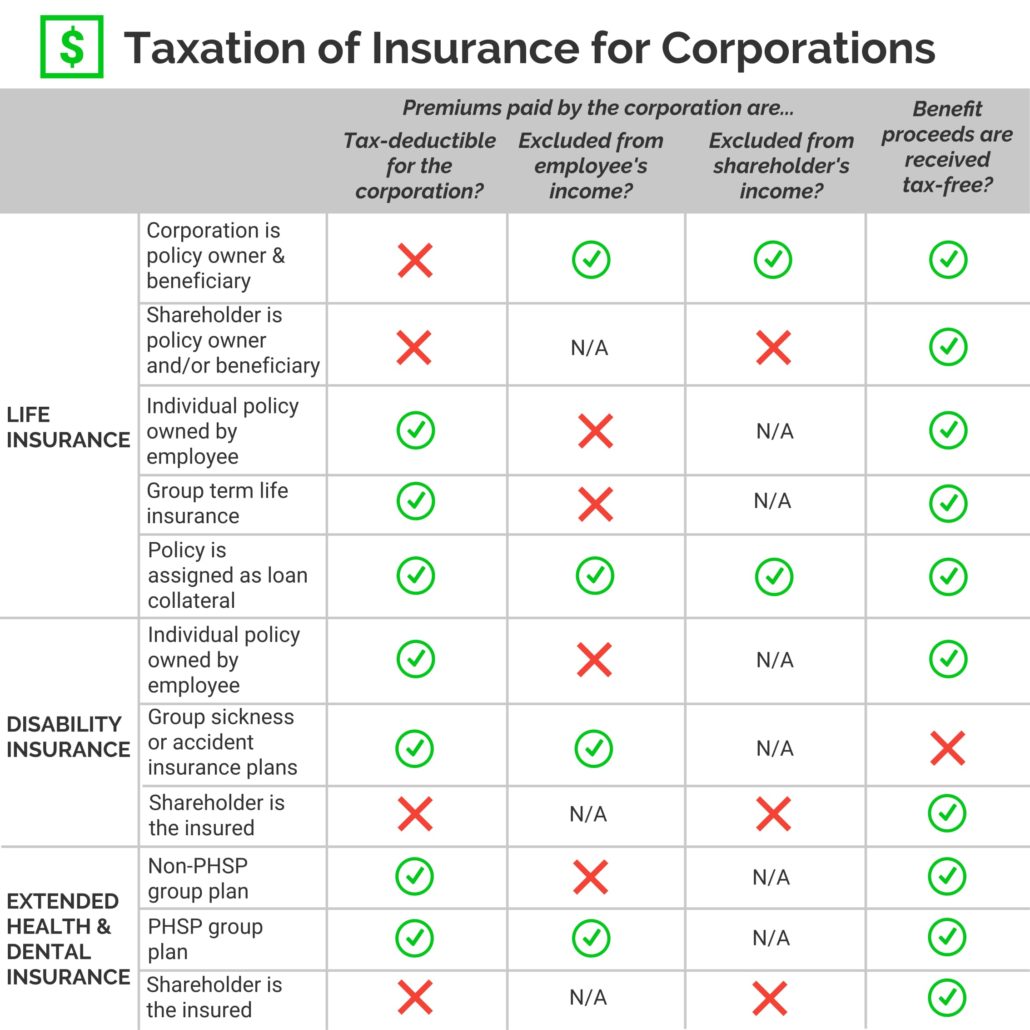

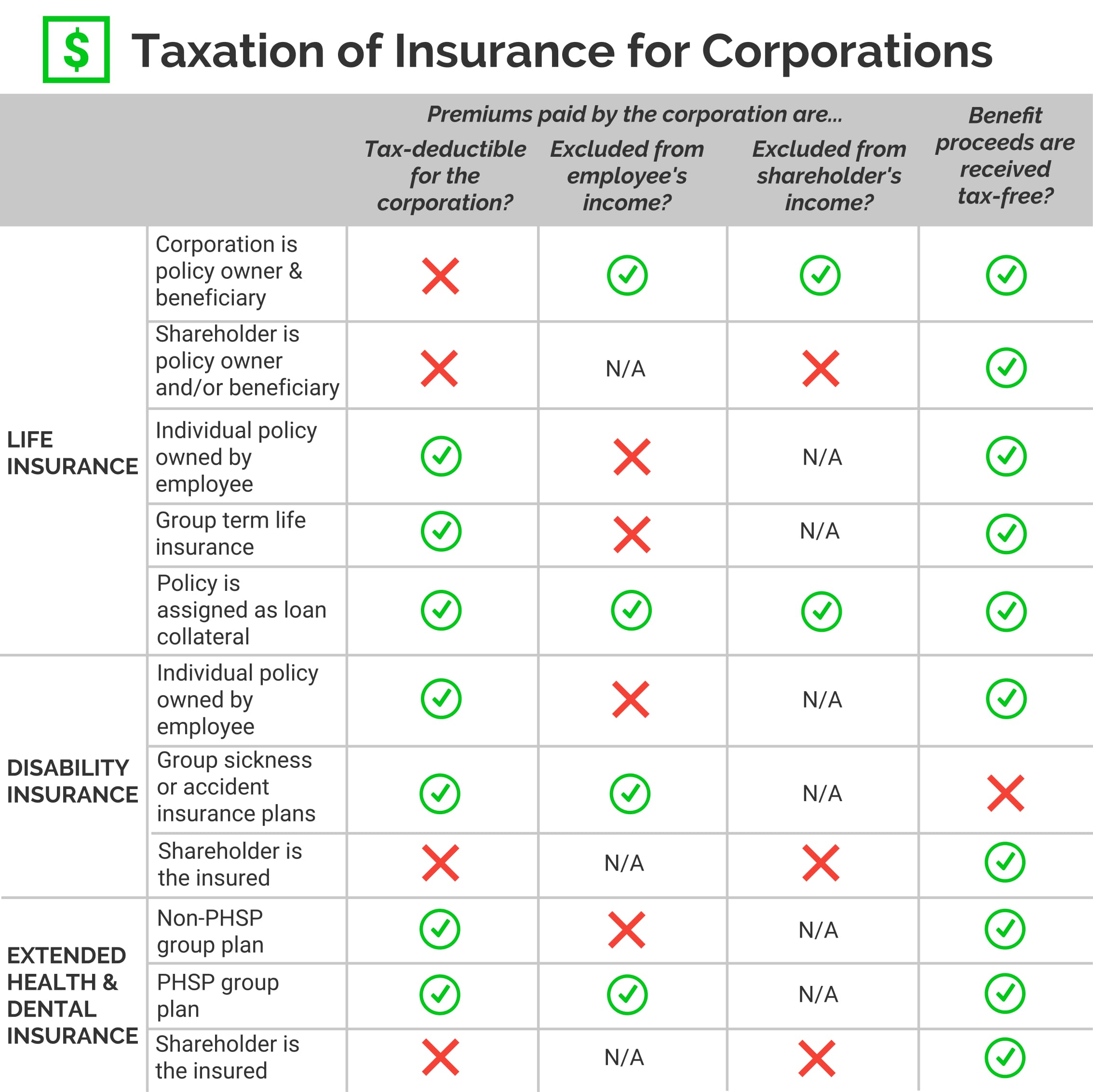

Life Insurance

If the corporation owns the life insurance policy and is its beneficiary, it can pay the life insurance premiums and collect the proceeds upon the death of the covered person. The corporation cannot deduct the premiums as a business expense, but since a corporation’s tax rate is usually lower than the personal tax rate, it’s likely still advantageous (i.e. cheaper) to fund the premiums with corporate dollars rather than paying for it personally. Proceeds are received tax-free to the corporation and an equivalent amount (net of the adjusted cost basis) is added to the company’s capital dividend account which can then be paid out tax-free to shareholders as a capital dividend.

If a shareholder owns the policy, corporate-paid premiums are included in the shareholder’s income as a shareholder benefit and are not deductible for the corporation. Benefit proceeds are still collected tax-free.

If an employee owns the policy, corporate-paid premiums are included in the employee’s income as a taxable benefit, but may be deducted against the corporation’s business income provided the premiums are a reasonable business expense. Again, benefits are collected tax-free. Note this applies for group term life insurance as well as for individual life insurance policies owned by an employee where premiums are paid by the corporation.

Another case where corporate-paid life premiums may be tax-deductible is when the policy is assigned to a financial institution as collateral security for a loan. If certain criteria are met (e.g. the lender requires the collateral assignment as a condition for granting the loan, interest on the loan is deductible, etc.) then the corporation is allowed to deduct the lesser of the premiums and the net cost of pure insurance.

Disability Insurance

When a corporation pays premiums for an individual disability insurance policy owned by an employee, the premium is added to the employee’s income as a taxable benefit and can be deducted by the corporation as a reasonable business expense. Benefit proceeds are not taxable.

For group sickness or accident insurance plans (i.e. a group of disability insurance policies owned and premium-paid by the corporation with benefits directly payable to employees), corporate-paid premiums are not considered taxable employee benefits and are tax-deductible to the corporation. However, any disability benefits collected in the future will be taxable to employees. Because of this, experts typically advise employees to pay for disability insurance themselves via payroll deductions so that they receive a taxable benefit for the premiums but the benefit amount becomes non-taxable.

Note that in owner-manager situations, different tax consequences will result if disability coverage is received by the insured in his/her capacity as a shareholder rather than an employee. Premium payments will be included in the shareholder’s income with no deduction to the corporation, and benefit proceeds will be non-taxable.

Extended Health and Dental Insurance

In general, corporate-paid premiums are treated as taxable income for the employee and can be deducted as a business expense by the corporation. The only exception are premiums paid towards private health services plans (PHSPs), which are not included in the employee’s income but are still tax-deductible for the corporation.

Benefit proceeds are received tax-free. Any portion of the premiums paid by the employee qualifies as a medical expense of the employee in calculating their medical expense tax credit on their personal income tax return.

For the above to apply in owner-manager situations, a shareholder must receive the benefit in his/her capacity as an employee, not as a shareholder. This means he/she must be actively engaged in the business activities of the corporation, and the benefits must be reasonable and consistent with what would be offered to an arm’s length employee providing similar services. If not, the premiums payments will be included in the shareholder’s income and be non-deductible to the corporation, and benefit proceeds remain tax-free.

Conclusion

As you can see, the tax treatment of premiums and benefits of insurance policies depends on various specifics such as the purpose and ownership of insurance, status as a shareholder vs. employee, etc.

Do you want to make sure your corporation is achieving optimal tax efficiencies for insurance payments?

We’re here to help! Contact us today and a licensed accounting and tax professional will be in touch to help you take a closer look.